An overview of the latest key information on the performance of the State's resources industry.

Major commodities review 2022-23

Western Australia’s resources sector delivered yet another sales record of $254 billion in 2022-23.

This compares to previous records of $251 billion in 2022 and $234 billion in 2021-22.

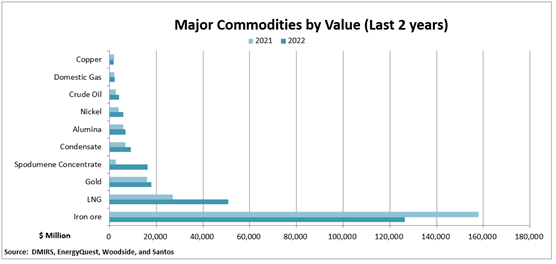

While down on recent levels due to lower prices, the iron ore industry still achieved an historically high sales value of $125 billion supported by record production of 861 million tonnes (Mt).

The fall in the value of iron ore sales was offset by growth in the value of liquified natural gas (LNG) and lithium sales.

Record high prices, particularly during the second half of 2022, and production translated into an all-time high Liquefied Natural Gas (LNG) production value of $56 billion (almost $18 billion more than in 2021-22 and more than $2 billion greater than the previous high in 2022).

Supported by record high prices and expanding production, the value of lithium (spodumene concentrate) sales increased to a record $21 billion, making it the State’s second most valuable mineral after iron ore.

The result was also supported by strength in several other commodities:

- Gold sales were valued at a record $18.6 billion on the back of the highest Australian dollar prices in history.

- The value of nickel sales was $5.7 billion, which is among the highest levels in the last 15-years and was achieved largely due to historically high prices, particularly in late 2022 and early 2023, as well as a rebound in production.

- Domestic gas sales were at an all-time high of $2.5 billion on a combination of rising prices, due to higher demand and a shortfall in production.

- Salt sales were a record $714 million due to increased prices.

The value of some other major commodities including condensate ($8.6 billion), alumina ($6.7 billion), and mineral sands ($1.4 billion) remained around the same level as in recent years.

The sector was also assisted by an overall weaker Australian dollar (as most commodities are priced in US dollars). It averaged 67 US cents for the financial year, down seven per cent on 2021-22, due to strength in the US dollar and financial market volatility.

Minerals

Minerals production was once again the dominant economic activity in the State’s resources sector with $183 billion in sales. However, this was down on recent years.

It accounted for 72 per cent of all resources sector sales, below the long-term historical average.

Iron ore sales were valued at $125 billion, down from record levels in recent years, and the major reason for the overall decline in the value of minerals production.

However, it was still high in a historical context and the industry remained the backbone of the resources sector in Western Australia.

Across most of the second half of 2022, iron ore prices were in decline. They fell below US$100 per tonne as China’s Government remained committed to its COVID-zero policy. They subsequently improved following an easing of China’s COVID-19 related restrictions, economic stimulus including to support an ailing property sector, as well as restocking by Chinese steel mills. However, this was not enough to offset the earlier losses.

There was 861 Mt of iron ore sold from Western Australia, the highest quantity on record for a single calendar or financial year. It was supported by a recovery in sales from Rio Tinto’s operations due to operational improvements and the ramp-up of Gudai-Darri, which achieved nameplate capacity in the June quarter 2023, as well as another year of record sales and shipments from Fortescue.

The iron ore industry’s share of sales was down on previous years, but it still accounted for 68 per cent of all mineral sales and 49 per cent of total resources sales.

Lithium (spodumene concentrate) sales increased to a record $21 billion supported by higher prices and tonnages, which elevated it into the position of Western Australia’s second most valuable mineral by sales after iron ore. Spodumene concentrate spot prices increased to almost A$10,000 per tonne in the second half of 2022 as lithium demand continued to outstrip supply, supported by Government policies to encourage the sale of Electric Vehicles (EVs), particularly in China. Prices eased across the first half of 2023 with the removal of EV tax concessions in China, though still remained higher than at any other time prior to 2022.

Lithium (spodumene concentrate) sales volumes were the highest on record at 3.19 Mt with the ongoing optimisation of processing facilities and the completion of ramp-up of the Tailings Retreatment Plant at Greenbushes, the ramp-up to nameplate capacity of the Ngungaju plant at Pilgangoora, the ramp-up of Wodgina, and the expansion of production capacity at Mount Marion.

Gold sales increased to a record $18.6 billion. The average price of gold was stable year-on-year in US dollar times but increased in Australian dollar terms. It trended higher over the year on concerns about the global economy and fears of a recession, peaking at more than US$2,000 per ounce in April (and almost A$3,000 per ounce in May), before easing on signals of further interest rate rises in the United States. In volume terms, there was 6.8 million ounces (212 tonnes) of gold sold in the State, around the same level as recent years.

Alumina sales value remained steady at $6.7 billion despite lower production. Prices declined through the second half of 2022 on excess supply in the Asia Pacific market following the ban of alumina exports to Russia, as well as an increase in China’s domestic alumina production, while downstream demand remained suppressed by China’s ongoing COVID-zero policy. Local production was at the lowest level in 10-years (13.1 Mt) with Alcoa affected by lower bauxite grades, maintenance, as well as a gas supply interruption, while South32 was affected by energy supply challenges and planned calciner maintenance.

The value of nickel sales was $5.7 billion, amongst highest levels in the last 15-years. Nickel prices ended the financial year around the same level as where they started it. However, this masked considerable volatility. Prices rose sharply in late 2022-early 2023 on supply issues, particularly in Indonesia, as well as the easing of COVID-19 related restrictions in China. However, prices declined thereafter on concerns about a supply surplus following Tsingshan’s announcements that it will add Class 1 nickel to its production mix, the failure of Chinese demand to rebound following the cessation of its COVID-zero policies, and a strengthening US dollar. Local sales tonnages increased from:

- Nickel West due to an increase production of concentrate and matte products and inventory drawdowns which offset a slower than planned ramp-up of the Kwinana refinery following maintenance in late 2022 and heavy rainfall at Mt Keith operations in early April 2023.

- Scheduled major maintenance at Murrin Murrin in 2021.

- Ravensthorpe following improved ore handling and processing from the new Shoemaker-Levy deposit as well as improved beneficiation plant availability and stability.

- Savannah in the Kimberley, supported by record production in the second half of 2022 and despite several issues in the first half of 2023, including damage to its logistics route to site via the Fitzroy River Bridge, and technical challenges.

Conversely, IGO’s production was down from Nova, due to an 18-day suspension following a fire at the diesel power station in December, and Forrestania due to several seismic events that restricted access to higher grade areas.

Copper sales were valued at $1.4 billion, down one quarter. This was mostly due to lower sales volumes as the DeGrussa operations approached end-of-life, with processing transitioning to low-grade surface ores and stockpiles until no longer viable. The yearly average price declined on US interest rate rises and concerns about global economic growth amid bank failures, as well as a weak demand from the construction sector in China initially due to its COVID-zero policy and then a slower-than expected recovery in demand following the relaxation of the restrictions.

The remaining significant other mineral sales included:

- Mineral sands – $1.4 billion (the highest on record).

- Salt – $714 million (the highest on record).

- Coal – $376 million (the highest on record).

- Cobalt – $368 million.

- Manganese – $298 million.

- Zinc – $265 million.

Petroleum

The petroleum sector, comprising LNG, condensate, crude oil, domestic gas and LPG production, achieved sales valued at a record $71 billion.

The sector’s share of total mineral and petroleum sales was 28 per cent.

LNG was the most valuable petroleum product with production valued at a record $56 billion, followed by condensate at $8.6 billion (the 2nd highest level of all-time), crude oil at $3.1 billion (down on 2022, but still high in the context of the last decade), domestic gas at a record $2.5 billion, and LPG at $720 million (around the same level as recent years).

After increasing through the first half of 2022 to peak at around US$120 per barrel in mid-2022, oil prices trended down on increasing supplies from major producers including OPEC, as well as concerns about global economic growth which stifled demand. They were, overall, fairly stable year-on-year.

A record peak for LNG prices of nearly US$19 per million British thermal units (mmbtu) was not reached until September 2022 as gas supply concerns, particularly in Europe, saw previous importers of now-sanctioned Russian gas seek alternative sources of supply in the Asia Pacific market (the main market for LNG from Western Australia), and Japan, China and South Korea secured supplies ahead of winter. Prices moderated through the first half of 2023 on muted demand and solid inventories in major importing nations. The result was higher average LNG prices compared to 2021-22 and a similar average to 2022.

LNG production was at its highest level on record (49.7 Mt) with all Western Australia facilities reporting a year-on-year increase in output. The result largely reflected the ongoing outperformance of Wheatstone and Pluto, with the North West Shelf also performing better via the start-up of the Pluto-Karratha Gas Plant Interconnector. Gorgon was impacted in the June quarter 2023 by the tie-in of new wells to maintain supply volumes.

Condensate production was 11.7 GL, a decrease from 12.1 GL in 2021-22 but still at a historically high level. This decline largely reflected a fall in output from the Ichthys floating production, storage and offloading (FPSO) facility and the North West Shelf as legacy gas fields decline.

Oil production was 3.4 gigalitres (GL), the first time it has dropped below 4 GL in five years and continuing a slow decline from the record levels of 15 to 20 years ago. This was due to largely to the shutdown of Enfield/Vincent with the Ngujima-Yin FPSO departing for planned maintenance in the first half of 2023.

For an overview of the overall performance of the resources sector against key indicators, please see the mineral and petroleum economic indicators 2022-23.

For more information on Statistics Digest

For more information on the Annual Report